By: Apostolopoulos Dimitrios & Valici Thomas

The Greek banks have been under regulatory and ECB pressure to reduce their exposure to NPLs since high exposure to NPLS is something that restricts their ability to expand credit and help the economy’s recovery. In terms of concrete policy actions many suggestions have been made (including the creation of a “bad bank” that will gather all NPLs). Until today, however, the process is the following.

Through an internet platform set up by banks, investment funds bid to purchase pools of NPLs. The highest bidder would acquire the package. Those pools of loans are made up by banks themselves. Intermediaries (mostly consulting and financial intermediaries firms) would help investors to value and collect a percentage of the loans. In Cyprus, one of the Big Four accounting firms has already published a report on this while European and American funds (many of them based in Luxembourg) have already shown considerable interest.

In June 2018, Reuters reported a deal that had been made between APS Holdings and Piraeus Bank for an amount ranging from 4.5 to 5.5% (18 to 22 million of euros) of a pool (called Arctos) consisting of unsecured consumer loans. Originally valued at 2.3 billion euros, it had been depreciated by over 80%, and was listed for a total amount of 400 million euros on the bank’s balance sheet. Half of that pool was composed of 1,000 to 5,000 euros range consumer loans. With this huge margin of safety, investment funds are planning to make a 4 to 5% minimal profit.

Earlier this year, Ultimo Portfolio Investment (Luxembourg) S.A. (part of the B2Holding group) reached a deal with Alpha bank for a pool of NPLs (mostly consumer), originally valued at 3.7 billion euros, for 90 million euros. Despite this huge discount, the benefit for the banks is that their overall capital requirements will be reduced, “freeing” capital for productive investments.

Since European governments are more indebted than they were, their ability to recapitalize banking institutions is considerably reduced. At the same time, it will be more and more difficult for them to politically justify a bail out to their electorates. In addition to that, the ECB is pressuring European banks to clean their balance sheets by selling bad loans. As a result, banks are forced to discount the price of their assets with the shareholders absorbing the loss. This process might be repeated in other European countries that exhibit high exposure to non-performing loans (e.g. Cyprus, Portugal, and Italy).

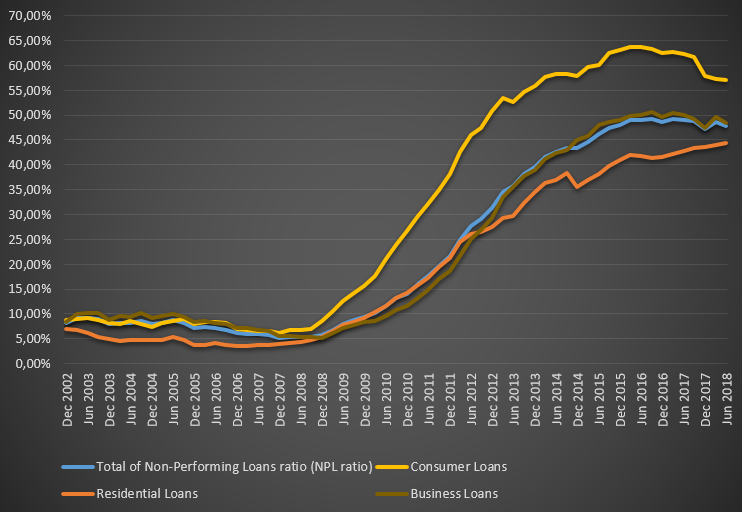

FIGURE 1

Evolution of non-performing gross-loan ratios in Greece (12/2002 – 06/2018)

Source: Bank of Greece

To read the entire blog, download the PDF by clicking on the button.

Articles liés

Tableau de bord économique et social – Septembre 2024

Tableau de bord économique et social – Septembre 2024- “Si j’étais formateur du Gouvernement…” – retour en vidéo sur l’événement du 13 juin.

- Les entreprises luxembourgeoises investissent-elles suffisamment dans la R&D ?

- Un étésien d’optimisme ?

- Les grandes trajectoires du Grand-duché

- -8% dans les Big Four : Simple trou d’air ou signal d’alarme ?