Two years ago, on the 20th of June in 2016, a remarkable exhibition opened its doors at the Acropolis Museum in Athens. The exhibition’s title was “Dodona. The oracle of sounds” and its aim was to provide wider knowledge about the oldest (ancient) Greek oracle. From this exhibition comes the photo above, one of the thousands of questions carved into metal sheets of lead that were found in excavations in Dodona. In the sheet, which dates back to the late 5th – 4th century BCE, someone’s asking if it would be better for him to pay off his debts immediately or leave them for latter. Unfortunately, we don’t know the Oracle’s response. What we do know however, is that debt -and the woes accompanying it- is a tale as old as time. Let us now take a leap of about 2500 years and arrive at today’s Greece.

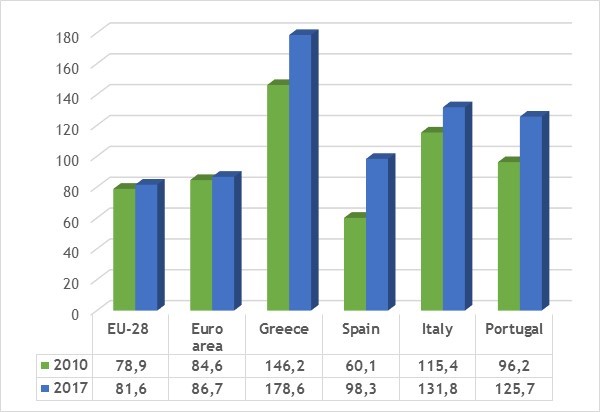

FIGURE 1

General government gross debt – annual data / Percentage of gross domestic product (GDP)

Source: Eurostat [sdg_17_40]

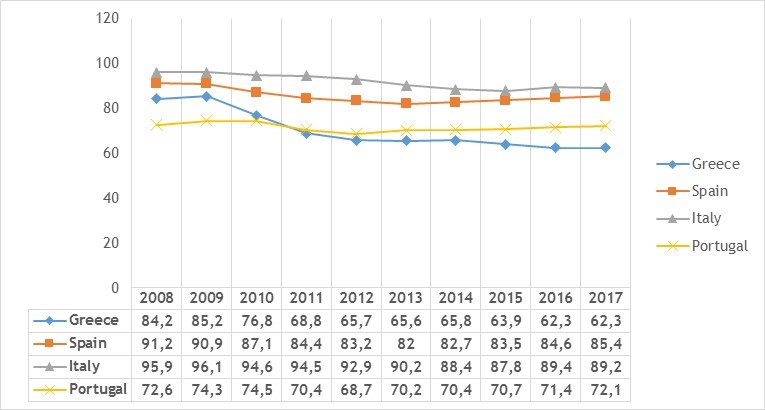

The 2010s have not been a great decade for nearly anyone –far less for Greece. Between 2008 and 2013 GDP declined by 26% and then stagnated for the following years (+0.1% in 2013-2016)[1]. Relative living standards (GDP per head compared to the west European average, Figure 2), having risen from 74% in 2000 to 85% in 2009, fell to 62% in 2016 (below their 1961 levels).

Employment levels and disposable incomes fell while poverty rates skyrocketed. The magnitude of the Greek crisis has been staggering.

FIGURE 2

GDP at current market prices per head of population in purchasing power standards, relative to the EU-15 average

Source: AMECO Eurostat

The magnitude and the impact of the crisis on everyday life in Greece caused such a political upheaval that discredited the parties that ruled the country since the restoration of democracy (1974)[1] and led (in January 2015) to the election of an anti-austerity coalition that ended signing up a third (and largely unnecessary[2]) austerity program (in July 2015) –just a week after the voters had rejected a version of it in the referendum of the same month. The view that Greece might be better off outside EMU (that had already been circulated by Wolfgang Schäuble)[3] had already gained some popularity. Prominent economists (that, alas -and with the deepest respect for their intellectual stature, had little –at best– experience or knowledge of the workings of the Greek economy and of the Greek political system and society –and to use Nassim Taleb’s words, had no “skin in the game”) urged Greeks to reject the bailout program at the July 2015 referendum either because the uncertainty and the deterioration of the living standards that would follow a Grexit would still be better than “the policy regime of the past five years” (Krugman) or than “the unconscionable torture of the present” (Stiglitz). In the European political world, the supporters of a “No” were of a rather different flair. Marine Le Pen, UKIP’s Nigel Farage and Matteo Salvini of Italy’s “Lega Nord” had all been very vocal in their public encouragement to Greeks that would vote for a “No”. Within Greece, however, opposition to the Euro was never popular, with 27% of the population being against the Euro and 69% being in favor[4].

It is not the aim of this note to offer an overview of the content, implementation and success (or lack of it) of the Economic Adjustment Programs for Greece. I will also not argue weather Greece has exited the crisis for good or not[5] (though the answer seems quite obvious if we look at Figure 1). Greece has (narrowly) averted Grexit in 2015. If it is going to be back on the negotiating table is something I don’t know though I doubt it (for the foreseeable future). After Le Pen’s failure to be elected President of France in 2017 and with Salvini’s referendum on exiting the Euro appearing to be a “no go”, the relevance of a scenario of exiting EMU seems reduced but, nonetheless, the argument that a Grexit will not solve Greece’s problems might be relevant to public debates in Europe[6]. In any case, in order to solve Greece’s (and Eurozone’s) problems, one must first identify the crisis’ true causes and setting the record straight is a move towards that direction.

TO READ THE ENTIRE BLOG PLEASE CLICK ON THE BLUE BUTTON

[1] The most prominent example here is that of the Greek social-democratic party (PASOK) that dominated Greece’s political life in the period known to Greeks as “Metapolitefsi” (1974-2010?), forming consecutive governments and ruling the country in 1981-1989, 1993-2004, and 2009-2011. PASOK saw a declining share of the vote in national elections from 43.92% in 2009 to 4.68% in 2015 and provided inspiration to journalists and academics for coining a term that describes the decline of social-democratic political parties in Europe (Pasokification). PASOK was the main but not the only Greek party that saw the decline of its popularity (and votes). New Democracy (the center-right party that was the main responsible for the restoration of democracy in 1974, and is the other major party in Greece’s two-party system) saw a declining share of the vote in national elections from 41.84% in 2007 to 27.81% in 2015. It is telling that while in the election of 2007 these two parties gathered 79.94% of the votes, in 2015 their combined percentage was just 34.49% (slightly improving in the second round with 34.38%).

[2] According to Klaus Regling (19.08.2018), Chief Executive Officer of the European Financial Stability Facility (EFSF) and Managing Director of the European Stability Mechanism (ESM), the first half of 2015 (when the so called “negotiation” of Greece with its creditors took place) cost Greece €86-200 billions. See also a speech by Yannis Stournaras, Governor of the Bank of Greece, at the Conference organized by the Hellenic Observatory of the London School of Economics on “Getting Policy Knowledge into Government”, London, 19 May 2016. “(…) [Nikos Theocarakis] failed though to admit that the “brave” negotiations that he and Yanis Varoufakfis led, which led to the change of the name of the Troika to institutions and removed the Troika from the ministries to the Hilton, had also a cost. If we assume that what he described were benefits, the cost of course was €86 billion: That was the third memorandum and the capital controls that have been imposed after €45 billion of deposit outflows. And these capital controls have been imposed in order to safeguard financial stability following the “brave” negotiations of Mr. Theocarakis and Mr. Varoufakis. I am sorry to say that, but I had the obligation to put the record straight.”

[3] See also Spiegel’s more dramatic exposé of the negotiation period between Greece and Germany.

[4] With the opposition to a “European economic and monetary union with a single currency, the Euro” in Italy, Spain and Portugal being 29%, 19% and 15% respectively. Source: Standard Eurobarometer 89, March 2018.

[5] For some (early) accounts on the ambiguous success of the bailout programs see here, here, and here. Some of the most insightful accounts have been written (perhaps not surprisingly) in Greek (Pagoulatos and Ioakeimidis).

[6] See also Iordanoglou and Matsaganis (2017) on the same topic.

[1] Spain (-8.9%), Italy (-7.6%) and Portugal (-7.8%) have all experienced a less deep recession over the same years and, since then, experienced a recovery of +7.9%, +1.8% and 3.9% respectively. Source: Eurostat [nama_10_gdp].

Articles liés

Idée du mois n°6 – 2015: La zone euro encore un machin, bientôt une machine ?

Idée du mois n°6 – 2015: La zone euro encore un machin, bientôt une machine ?- Recherche, développement et innovation : les défis du Luxembourg

- La Fondation IDEA asbl fait peau neuve !

- Non, tous les travailleurs ne sont pas en télétravail.

- Quels besoins en logements au Luxembourg ?

- Cahier thématique n°2/5 – Europe